If you are looking to deploy ₹10 lakhs today, the real challenge isn’t finding options—it’s deciding what to do with them.

There’s no shortage of advice. Every day there’s a new “best investment,” a new trend, or a new prediction about where markets are headed. But very little of that helps with a simple, practical question:

How should I actually allocate my money?

Instead of trying to pick the “perfect” investment, it helps to step back and think in terms of structure.

Why Allocation Matters More Than Selection

A lot of people spend time trying to choose the right stock, the right fund, or the right asset.

But in reality, long-term outcomes are often driven more by how money is allocated across asset classes than by any single investment choice.

Getting that structure reasonably right:

- Reduces risk

- Brings stability

- Makes it easier to stay invested

And most importantly, it removes the need to constantly react to market noise.

A Simple Way to Think About ₹10 Lakhs

The exact allocation will always depend on individual goals, time horizon, and risk comfort. But as a starting point, it helps to think in terms of a few basic buckets:

- Growth

- Stability

- Hedge

- Flexibility

This keeps things simple without being simplistic.

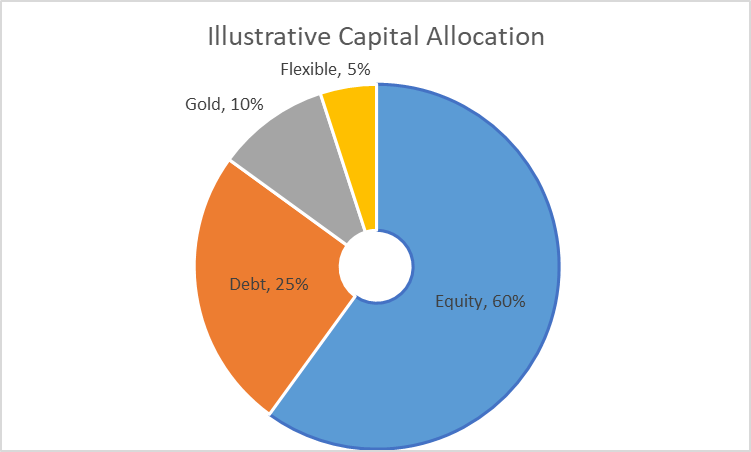

An Illustrative Allocation

For illustration, a balanced approach could look something like this:

- ₹6,00,000 → Equity (growth)

- ₹2,50,000 → Debt (stability)

- ₹1,00,000 → Gold (hedge)

- ₹50,000 → Flexible / opportunistic

This isn’t a prescription—it’s just a way to visualize how different roles can fit together.

Breaking It Down

Equity (Growth)

Equity typically forms the core of long-term wealth creation.

It comes with volatility, but over time, it has historically been one of the more effective ways to grow capital.

For most working professionals, broad exposure (for example, diversified or index-oriented approaches) tends to be simpler and more manageable than trying to pick individual winners.

Debt (Stability)

Debt plays a different role.

It doesn’t aim to maximize returns, but it helps:

- Stabilize the portfolio

- Provide liquidity

- Reduce the impact of market swings

This becomes especially important during uncertain periods, when having a stable component makes it easier to stay disciplined.

Gold (Hedge)

Gold isn’t about high returns.

It’s more of a hedge—something that can behave differently from equity and provide balance during certain economic conditions.

A small allocation is usually enough to serve this purpose.

Flexible Allocation

Keeping a small portion unallocated or flexible can be useful.

It allows you to:

- Take advantage of opportunities

- Adjust over time

- Avoid feeling “fully locked in”

Even a small amount can make a difference psychologically.

Adjusting Based on Risk

Not everyone will be comfortable with the same mix.

- A more conservative approach may lean more toward stability (higher debt, lower equity)

- A more aggressive approach may increase equity exposure

The key is not to find the perfect ratio, but to choose one that you can stick with over time.

Common Mistakes to Avoid

A few patterns tend to repeat:

- Putting everything into one asset class

- Chasing recent winners without a broader plan

- Ignoring the role of stability in a portfolio

- Overcomplicating with too many investments

- Reacting too quickly to short-term market movements

Most of these are less about knowledge and more about discipline.

Final Thought

There’s no single “right” way to invest ₹10 lakhs.

But having a simple structure—one that balances growth, stability, and flexibility—can go a long way in making investing more manageable.

In the long run, consistency and discipline tend to matter far more than getting every decision exactly right.

This article is for educational purposes only and does not constitute financial advice.

Abhishek writes about investing, asset allocation, and long-term wealth building with a focus on simplicity and practical decision-making.